Challenges facing the insurance industry

Band aid solutions won’t address today’s challenges.

By Martin Stewart : 9th of September 2019

Challenges are nothing new to the insurance industry. But while in the past transformation has taken years, now things may change in a matter of weeks. Confronting as it is, the threat of new disruptors has made many existing insurers consider how they will transform to become more customer-centric by changing their systems and processes. Beyond challenger brands there are yet more insurance industry challenges on the horizon. Adapting to these requires more than band-aid solutions. Insurers must rethink their approach from the ground up.

Legacy systems

Since the Global Financial Crisis forced insurers to focus on cost-cutting measures to weather the storm, moves to overhaul and modernise legacy systems have picked up speed. This has meant not only paying attention to their policy administration system (PAS), but also to every part of their underlying infrastructure – from sales to claims management, billing and collections.

Over two thirds of life insurance providers have already, or are in the process of, modernising their policy administration system.

Hiring the right skills

As the insurance industry has grappled with rapid change , new approaches to hiring are needed. Insurers need to ignore their subjective perceptions that lead them to hire people like themselves as this promotes the status quo over the ability to adapt to the market changes.

Modern insurance companies need: – Data scientists who can analyse big data – Diverse local workforces to help strengthen a presence in emerging markets – Adaptive workplace cultures to accommodate generational and cultural differences – Stronger leadership pipelines

Cyber security

Cyber security is a very real issue for large organisations, especially those that deal with sensitive and financial data like insurers. As technology becomes more pervasive, the amount of data collected and stored will include an ever-growing amount of personal information. Not only are there legal obligations to deal with this information appropriately but it is also a matter of reputational risk.

46% of APRA-regulated insurers report experiencing a cyber security incident in the past 12 months. 62% have tested their ability to respond to and recover from cyber-attacks.

Regulation and compliance

Insurers are constantly told that to adapt to a changing world they need to be agile, innovative and even revolutionary in their approach. However, the insurance industry faces unique challenges in trying to match the agility of other sectors, due to a highly regulated environment. This all increases not only the challenge but the cost of compliance for insurers, with 95% of financial service organizations expecting their compliance costs to increase next year.

One in ten insurers anticipate spending over 10% of their annual revenue to meet their regulatory obligations by 2023.

Technology giants

There are increased rumblings from tech giants like Apple, Google and Amazon that they may be looking to move into the insurance space. As margins in the insurance will improve dramatically with their technology the tech giants are likely to target high-volume, high-profit insurance products. This will leave legacy insurers with decreasing revenue, lower margin products, and crippling fixed costs.

This is particularly concerning when you consider what tech giants have that insurance companies haven’t:

- Strong direct consumer relationships

- Deep data and analytics

- Highly skilled talent with experience in AI and SaaS

- The ability to move very quickly.

Armed with direct consumer relationships and access to deep data, tech giants like Apple, Google and Amazon are poised to move into the insurance space.

Insurtechs are on the rise

On the flip side of the insurance coin are the smaller insurtechs that are nipping at the heels of legacy insurers. Many are cherry picking relatively simple and highly profitable products like mobile phone cover. Or, they are taking a direct-to-consumer approach through value comparison websites and peer-to-peer insurance. This allows them to easily pick out the 20% of business that makes 80% of the profits – a serious danger for established insurers. And some insurtechs are so well funded they can afford to run big losses for years while they are building up volume.

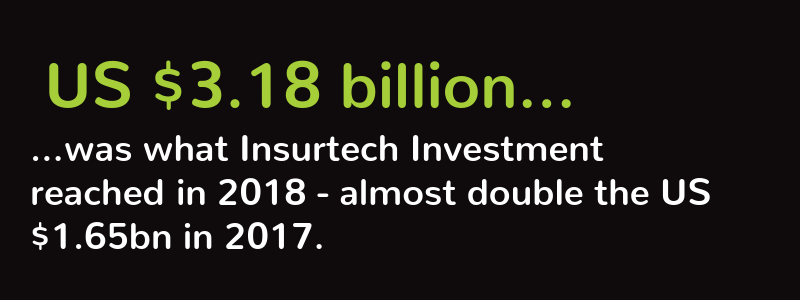

Investment in Insurtech reached US$3.18bn in 2018 – almost double the US$1.65bn in 2017.

With change comes opportunity

With so many challenges ahead, it’s understandable that many insurers feel overwhelmed. However, with change comes opportunity. Identify and leverage these opportunities and develop strategies to retain your competitive edge.

1. Big data and analytics

While insurance has always been a data-driven industry, consumer demand and technology have revolutionised both the scale and purpose of that data. With more information than ever at our fingertips, consumers are demanding more in return. Use data analytics to:

- Identify your core, profitable market segments

- Identify customers’ pain points

- Tailor your products to customers

- Develop new products bundles for new opportunities, such as the work from home market

- Build client relationships with personalised service

2. AI and digital transformation

AI and digital transformation aren’t just about delivering bespoke service – they’re allowing insurance companies to automate more of the process and dramatically reduce overheads. By embedding digital technology across your organisation, you can:

- Harness and use big data

- Streamline operations

- Reduce operating costs

- Improve customer experience

- Expand market share

Of those consumers who would prefer to buy insurance digitally, less than 50% of consumers do because insurers lack the capability.

3. Developing partnerships

Expand your digital capabilities and share their innovations and efficiencies by working together. Form joint ventures or purchase them outright (but be careful not to kill their innovative start up culture).

Conclusion

Successful insurance companies are already responding to current and future challenges by reimagining their strategy, business models, and processes from the ground up. From hiring new talent that can meet the insurance industry challenges to creating a digital culture that streamlines customer experience, there are many steps along the path to transformation. In today’s economy, meeting change head on is essential to your continued survival.